Global equity markets retreated sharply on Monday as a coordinated U.S. and Israeli military strike against Iran upended geopolitical stability, sending shockwaves through the travel and discretionary sectors.

In Europe, the Stoxx 600 Index fell as much as 1.9% at the open, while S&P 500 futures slid 1.7%, mirroring a 1.8% slump in the MSCI AC Asia Pacific Index.

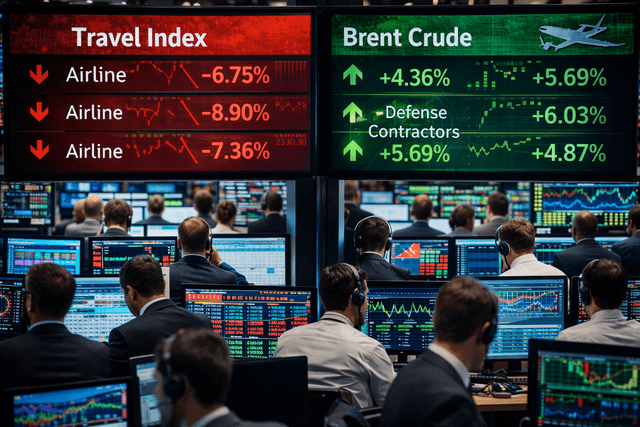

The market reaction highlighted a stark bifurcation between sectors vulnerable to rising costs and those positioned to benefit from a wartime economy.

Airline and hotel stocks were among the heaviest hit, with British Airways parent IAG SA and French hotel giant Accor SA leading the decline.

Investors are pricing in a dual blow of surging jet fuel prices—following a 13% spike in Brent crude—and widespread airspace closures across the Middle East.

Conversely, defense and energy stocks emerged as the sole beneficiaries of the volatility.

UK defense contractor BAE Systems and Norwegian oil major Equinor ASA saw significant gains as Western governments signaled a massive military buildup in the Persian Gulf.

Barclays strategist Emmanuel Cau described the current environment as "highly fluid," suggesting that the "quality theme" and commodity-linked stocks remain the most effective hedges against potential disruptions in the Strait of Hormuz.

The inflationary implications of the conflict have also triggered a rapid shift in regional preferences.

Citigroup upgraded UK equities to "overweight" on Monday, citing the FTSE 100’s heavy concentration in commodities and defensive sectors as a superior "geopolitical hedge."

Simultaneously, the bank downgraded Japanese equities to "underweight," citing the country's sensitivity to energy imports.