TransUnion Q4 earnings beat estimates, but 2026 outlook disappoints

TransUnion (NYSE:TRU) shares fell 2.5% in pre-market trading Thursday, despite the credit reporting giant delivering a "beat and raise" performance for the final quarter of 2025.

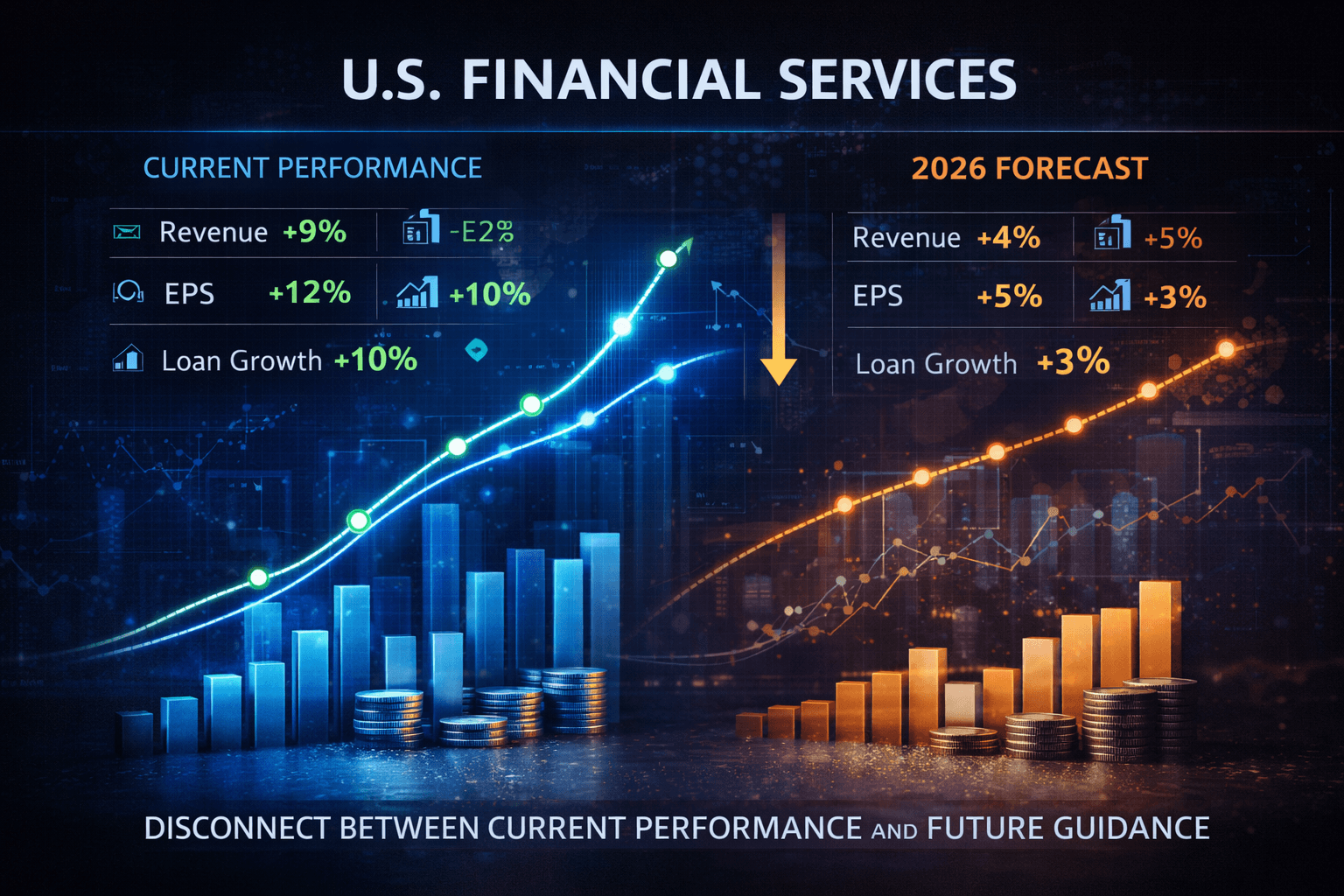

The data firm posted fourth-quarter revenue of $1.17 billion, a 13% year-over-year increase that outpaced the $1.13 billion consensus.

Growth was turbocharged by a 19% surge in U.S. Financial Services revenue, as a rebound in mortgage originations and steady auto lending drove higher inquiry volumes.

Adjusted diluted EPS for the quarter hit $1.07, landing well above the $1.03 analysts expected.

However, the stock faced pressure as management’s initial 2026 outlook appeared to prioritize "prudent" targets over the double-digit momentum seen in Q4.

For the full year 2026, TransUnion expects adjusted diluted EPS of $4.63 to $4.71, coming in below the $4.86 Wall Street estimate.

While the company is targeting robust 8–9% revenue growth, investors are weighing the impact of a potential labor market slowdown on consumer credit health.